Auto Loan Calculator

Calculate payments over the life of your Loan

Home Blog Privacy Terms About ContactCalculate payments over the life of your Loan

Home Blog Privacy Terms About ContactPublished on October 13, 2025

My journey into the weeds of loan calculations didn't start with a big financial goal or a sudden need for money. It started with a simple, offhand comment from a friend. We were talking about recent purchases, and they mentioned their new car loan. "The monthly payment is way lower than I expected," they said, "so I went with a longer term to keep it manageable." In my head, a little light bulb went off, but it was a dim, flickering one. Lower payment, longer term. It sounded logical, right?

But then the questions started bubbling up. If the loan amount and interest rate were similar to what I'd been looking at, how could the payment be so much lower? Is a lower payment always the better outcome? It felt like there was a piece of the puzzle I was missing, a mathematical truth hiding just out of sight. I wasn't interested in judging my friend's decision; I was genuinely curious about the mechanics behind the numbers. My goal became simple: I wanted to understand the relationship between the time you take to pay back a loan and what it actually costs you.

I decided to dive into some online loan calculators, not to shop for a loan, but to experiment. I wanted to see the numbers move and change as I adjusted the variables. This entire exploration is purely about my personal journey to understand how these calculations work. This is about understanding how calculations work, not financial advice. I just wanted to finally grasp the "why" behind the math that seemed so straightforward on the surface but felt so complex underneath.

My initial attempts were clumsy. I'd plug in a number, see a result, and not fully understand what it meant. I was like a kid playing with a new toy, pushing all the buttons without reading the manual. It was this initial fumbling that led me to the central confusion, the one that would ultimately lead to my biggest "aha" moment in personal finance literacy.

Armed with my curiosity, I opened a basic online loan calculator. My mission was to recreate the scenario my friend described. I decided to use a hypothetical loan amount of $18,350. I typed it into the "Loan Amount" field. Next, I entered a sample interest rate—let's say 6.8%—into the "Interest Rate" field. Then came the most important variable for my experiment: the loan term.

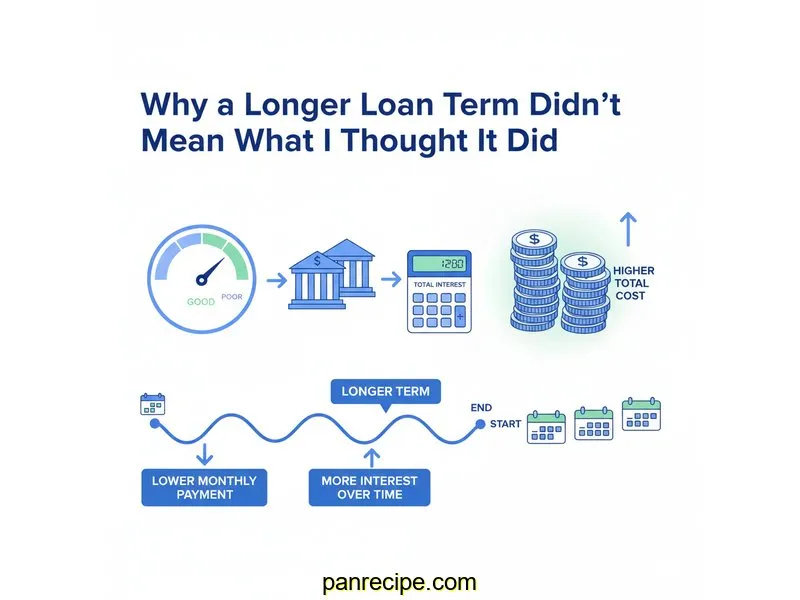

First, I put in a 48-month term (4 years), similar to what I had been considering. The calculator instantly spit out a result: a monthly payment of around $437.58. "Okay," I thought, "that's my baseline." Now for the interesting part. I kept all the other numbers exactly the same—$18,350 at 6.8%—but changed the loan term to 72 months (6 years), just like my friend's.

The new monthly payment appeared: $308.57. My initial reaction was a simple "Wow." That was a difference of nearly $129 every single month. My brain immediately jumped to the conclusion I think many people's would: the 72-month loan was clearly the "cheaper" option. My focus was entirely on that one, single number. I had found the answer to how my friend's payment was so low, and in my mind, the case was closed. I almost closed the browser tab right then and there.

This was my big mistake. I was so fixated on the monthly payment figure that I didn't even notice the other information the calculator was showing me. Fields like "Total Principal Paid," "Total Interest Paid," and "Total Cost of Loan" were just lines of text I completely ignored. I had solved for the variable I was curious about, but I hadn't yet understood the full equation. My narrow focus on one output meant I was completely missing the bigger, more important story the numbers were trying to tell me.

Something about my quick conclusion felt too simple. It gnawed at me. How could stretching out the payments result in a "cheaper" deal without some kind of catch? I went back to the calculator with a new sense of purpose. This time, I resolved to look at every single number on the screen, not just the one that answered my initial question.

I ran the two scenarios again. First, the 48-month term. Monthly Payment: $437.58. But this time, I forced my eyes downward. I saw a field labeled "Total Interest Paid." For the 48-month loan, it was $2,653.84. Then, I changed the term to 72 months. The monthly payment dropped to $308.57, just as before. But the "Total Interest Paid" number? It was $3,867.04.

That was it. That was the "aha" moment. My jaw literally dropped. To get that lower monthly payment, my hypothetical borrower would pay over $1,200 more in interest over the life of the loan. The "cheaper" monthly option was actually the more expensive loan overall. It wasn't a trick; it was just math I hadn't taken the time to see. The longer term gave the interest more time to accumulate. My friend wasn't getting a better deal; they were making a different trade-off: lower monthly cash flow strain in exchange for a higher total cost. Understanding this distinction felt like unlocking a new level in a game.

My entire framework for comparison shifted. Instead of asking "Which monthly payment is lower?" I started asking "Which total interest paid is lower?" The goal was no longer just about fitting a payment into a monthly budget but understanding the complete financial picture of the loan from start to finish. This felt like a monumental step in my financial literacy journey.

The core lesson was that interest isn't a one-time fee; it's calculated on the remaining balance over time. By extending the loan from 48 to 72 months, I was adding 24 more periods during which interest could be calculated. Even though the rate was the same, the extended duration meant the lender was earning interest for two extra years, which translated directly into a higher total cost for the borrower.

Curiosity got the better of me, and I finally clicked the "Show Amortization Schedule" button. It was like seeing the loan's DNA. For the 72-month loan, I saw that the very first payment of $308.57 included about $103.98 of interest and only $204.59 of principal. For the 48-month loan, the first payment of $437.58 also included $103.98 of interest, but paid down $333.60 of principal. Seeing this breakdown made it crystal clear how a shorter term attacks the principal balance much more aggressively from the very beginning.

To really cement this new understanding, I spent another hour playing with the numbers. I tried a 36-month term, a 60-month term, and even an 84-month term. Each time, the pattern held true: as the term got longer, the monthly payment decreased, but the total interest paid relentlessly climbed higher. I was no longer just seeing numbers; I was understanding the relationship between them.

After my deep dive, I came away with a new set of personal principles for how I look at loan calculations. It's not about what's "good" or "bad," but about being fully aware of what the numbers mean. This mental checklist has been invaluable for me, and it's all centered on calculation literacy.

Throughout this process, several questions popped into my head that I had to work through. Here are a few that were central to my journey of understanding.

I learned this is because interest is calculated on the outstanding balance periodically (usually monthly). With a longer loan, the principal balance decreases more slowly. This means that for a larger number of months, you're paying interest on a higher balance than you would be with a shorter-term loan, even if the interest rate is identical.

From a pure calculation perspective, I learned that while total interest shows the overall cost, the monthly payment is the key indicator of cash flow impact. Sometimes, a person might need to prioritize a lower payment to fit within a strict monthly budget, even if they understand it will cost more in the long run. The key discovery for me was not that a lower payment is "bad," but that it represents a trade-off between monthly affordability and total cost. The math simply illuminates that trade-off.

My process now is to keep the loan amount and interest rate constant and only change the term. I create a simple table for myself, noting the term (e.g., 36, 48, 60, 72 months), the resulting monthly payment, and—most importantly—the total interest paid for each scenario. This side-by-side comparison makes the relationship between the variables incredibly clear.

The amortization schedule showed me this clearly. Your interest payment is calculated by applying the periodic interest rate to your current outstanding balance. At the beginning of the loan, your balance is at its highest, so the interest portion of your fixed payment is also at its highest. As you pay down the principal, the balance shrinks, and so does the amount of interest you owe each month, allowing more of your payment to go toward principal.

My biggest takeaway from this entire exercise was a fundamental shift in perspective. I went from seeing a loan's cost through the narrow lens of a monthly payment to seeing it through the wide-angle lens of total interest paid over time. It's not about judging one approach as better than another, but about having the clarity to understand the full implications of the numbers in front of me.

This journey started with a simple question about a friend's car payment and ended with a much deeper appreciation for the mechanics of borrowing. It empowered me to look beyond the surface-level numbers and understand the story they tell. The calculator went from being a simple answer machine to a powerful learning tool that helped me connect the dots between time, cost, and affordability.

I'd encourage anyone who's curious to do the same. Don't just look for an answer; play with the numbers. Change the variables and watch how everything else reacts. It’s in that process of experimentation that true understanding is built. Gaining confidence in how these calculations work is a huge step toward feeling more in control of your financial literacy.

This article is about understanding calculations and using tools. For financial decisions, always consult a qualified financial professional.

Disclaimer: This article documents my personal journey learning about loan calculations and how to use financial calculators. This is educational content about understanding math and using tools—not financial advice. Actual loan terms, rates, and costs vary based on individual circumstances, creditworthiness, and lender policies. Calculator results are estimates for educational purposes. Always verify calculations with your lender and consult a qualified financial advisor before making any financial decisions.

About the Author: Written by Alex, someone who spent considerable time learning to understand personal finance calculations and use online financial tools effectively. I'm not a financial advisor, accountant, or loan officer—just someone passionate about financial literacy and helping others understand how the math works. This content is for educational purposes only.